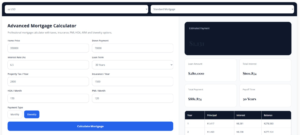

Loan Calculator: Estimate Monthly Payments and Total Cost

A loan calculator is a powerful tool that helps borrowers estimate their monthly payments and the total cost of any loan before applying. Instead of juggling spreadsheets or manual formulas, you enter a few key numbers – like the loan amount, interest rate, and term in years – and get immediate results. Our on-page loan calculator works just like leading tools from sources such as CFPB or university finance centers: you input the purchase price, down payment (if any), interest rate, and loan duration, and the calculator instantly shows your payment schedule. This simple process lets you compare scenarios and find a loan you can afford.

Using a loan calculator on our page saves time and avoids surprises. For example, Farmers & Merchants Bank’s mortgage calculator notes that it “determines your monthly payment and generates an estimated amortization schedule,” showing exactly how much of each payment is interest and principal. In practice, you can experiment with different interest rates and loan lengths to see what works best. As one mobile home lender explains, you can “try different interest rates and term lengths to find the right monthly payment for you,” just by entering the values and clicking Calculate. This makes it easy to answer questions like “What will my payment be if I refinance?” or “How does making a larger down payment change my rate?”.

How to Use the Loan Calculator

Our calculator is easy to use. You start by entering the loan amount (the price of the home or car, or the amount you need to borrow) and the annual interest rate (in percent). Then choose the loan term (how many years you will repay it). If applicable, enter a down payment or initial payment. Press Calculate, and the tool displays your monthly payment for principal and interest (P&I). This is exactly how most online mortgage calculators work. (You may add taxes, insurance, or extra payments separately, but our basic calculator focuses on P&I.) Some calculators also let you download an amortization schedule showing each year’s payments.

For example, the University of Nebraska’s Loan Payment Calculator asks users to enter the total purchase amount, down payment, interest rate, loan duration, and start year. It then computes the annual (or monthly) payment and can even output a PDF schedule. In the same way, our on-page calculator does the math for you instantly. You can change any input (say, raising the interest by 1% or extending the term by 5 years) and immediately see the effect on monthly costs. This interactivity makes planning easy: you can quickly adjust variables until you find payments that fit your budget.

Mobile Home and Manufactured Home Loans

Mobile and manufactured homes have their own financing quirks, and our calculator handles those too. If you’re buying a mobile home, you might need a down payment of 5%–20% depending on credit and whether the home is new or used. (New homes can sometimes qualify for as little as 5% down with excellent credit, while older models often require more.) The interest rate for a mobile home can also be higher than a traditional mortgage. Financial Services Unlimited notes rates “range from 7.4% to 12% depending on your credit quality, the age of the home, [and] loan type”. In our calculator, entering a larger down payment will reduce both your monthly payment and the total interest paid.

Consider a quick example: a $60,000 manufactured home at 8% interest for 20 years. Without a down payment, the monthly payment is about $502. But if you put down $10,000, you only finance $50,000, and the payment drops to about $418. Our calculator makes this clear instantly. You can even use it as a park model home financing calculator if your home is in a resort or RV park – the inputs are the same. For mobile homes on leased land (often called chattel loans), simply input the financed amount and term. For homes on your own land, it’s like a normal mortgage. In either case, the calculator gives you the payment and total cost in seconds, helping you decide how much house you can afford.

Farm, Land, and USDA Loans

Rural financing is another area where a specialized calculator is invaluable. A farm loan calculator or land loan calculator can show payments for acreage, equipment, or agricultural business loans. These often have longer terms or seasonal payment schedules. For example, a USDA rural home loan can offer 100% financing (meaning zero down payment for eligible buyers). Our calculator can handle zero down by simply setting the down payment field to $0. If you qualify for a USDA program, you get a “no money down” loan, and the calculator will show the relatively higher principal and interest payments that result.

Organizations like Farm Credit East highlight that their interactive farm loan calculator “can help you determine relative financing costs, based on your own inputs”. We achieve the same goal: you enter the loan terms specific to your farm operation or land purchase, and the calculator returns your payment schedule. This is handy whether you’re buying cropland, a ranch, or even refinance an existing farm loan. A land payment estimator works similarly for raw land purchases. In all cases, our on-page tool is a quick way to benchmark your options: if you change the interest or term, you immediately see how costs change, helping you plan and budget.

Auto Loans, Refinance, and Personal Debt

You can also use our calculator for non-home loans. For a car loan calculator refinance, enter your auto loan balance, the new lower rate, and a new term, and you’ll see if refinancing will truly lower your payment. Similarly, a standard auto loan or car loan calculator works the same way: just input the vehicle price (or loan amount) and get the payment. If you have credit card debt or a personal loan, our tool still applies. A credit card monthly payment calculator essentially uses the same math: enter the balance as the loan amount, an APR, and how many months to pay it off. The calculator then tells you the monthly payment needed or, if you enter a payment, how long it will take to clear the debt. This is especially useful for simple interest loans where interest accrues only on the remaining balance.

While our on-page calculator focuses on single loan scenarios, you might explore specialized needs too. For example, a reverse mortgage loan calculation is a bit different (it factors in age and home equity), but knowing your basic payment needs can guide that conversation. In short, any time you borrow money – whether for a vehicle, credit card, business equipment, or home – you can use this calculator to estimate costs. It’s like having a financial advisor in your pocket, instantly showing you the numbers.

15-Year vs 30-Year Loans

One classic comparison borrowers make is a 15-year loan vs 30-year loan. Shorter loans mean higher monthly payments but much lower total interest; longer loans give lower payments but cost more in interest over time. For example, on a $200,000 mortgage at 4% interest:

- A 15-year fixed mortgage would be about $1,479 per month, paying roughly $66,288 in interest over the life of the loan.

- A 30-year fixed mortgage on the same amount and rate would be about $955 per month, with total interest around $143,739.

The table below illustrates this difference clearly:

| Term | Monthly Payment | Total Interest |

|---|---|---|

| 15 years | $1,479 | $66,288 |

| 30 years | $955 | $143,739 |

By comparing these using our calculator, you see that the 15-year loan saves over $77,000 in interest compared to a 30-year loan. Of course, the 15-year payment is higher each month. As the CFPB points out, the type of loan (for example, a 15-year fixed vs 30-year fixed) is one of the key factors affecting what you can afford. You can test various combinations: perhaps a 20-year loan (not shown here) balances monthly cost and interest. Using the calculator, just change the term to see the new payment and total interest immediately.

Calculating Total Loan Cost

To find the total cost of your loan, simply add up all payments (including interest). In practice, you take the monthly payment output and multiply by the number of payments. For example, our 30-year mortgage above costs about $955 × 360 = $343,800 total; subtracting the $200,000 principal shows $143,800 in interest (roughly matches the table). Similarly, the 15-year loan costs $1,479 × 180 = $266,220 total, or $66,220 interest. (Small rounding differences aside, these examples show the math.) Many mortgage calculators – like Bankrate’s or ours – display the total loan payments and interest when you run a calculation. This lets you see the full impact of interest over time, not just the monthly check.

Always remember to include all costs: if your calculator doesn’t include taxes or insurance, add those to your monthly budget separately. And if you make extra principal payments or one-time fees, include those in your “total cost” calculation. In short, the loan calculator gives you the basics (principal and interest). Then add taxes, insurance, or HOA fees if needed to know the true full payment. That way, you’ll have a realistic picture of your expenses before signing any loan.